William Mougayar is a Toronto-based angel investor and four-time entrepreneur who advises startups on strategy and marketing. In the first of this three-part series, he discussed how banks dealt with the emergence of the Internet and how blockchain technology is causing these institutions a whole new headache. Here, in part two, he looks at why and how banks should start embracing blockchain technology.

Build on-ramps, not barriers

Banks can’t really pick and choose a small subset of use cases and claim they are embracing the revolution. If you use “blockchains without bitcoin” just to avoid public blockchains, you will be subjected to a huge market blind spot because there are millions of users that want to trade with bitcoin, and you’ll be insulated from them.

Bitcoin’s adoption does not seek permission from any bank or government. The cat is already out of the bag, and a new parallel financial environment is forming around it and other cryptocurrency-related technologies, powered by networks of computers that secure it, validate it, enforce it and run it.

If financial services were to be re-invented today from scratch, we would be fine with virtual, online, Internet and blockchain-enabled services. There would be no traditional bricks and mortar branches.

Instead of visiting a branch, we would do a video call with a remote service representative who can verify our identity, and it goes from there. Technically speaking, bitcoin, blockchains and their related ecosystem can replicate a bank today without much difficulty, both for consumer retail banking and business-to-business services.

Truth is, there will be pressure from consumers who are already getting a taste of freedom from banks via alternative FinTech services. Blockchain-enabled solutions will take that freedom bar even higher via decentralization, peer-to-peer behaviors, and by putting more power at the edges of the network directly in the hands of users, or by granting more processing power at the nodes of the computing networks and software applications.

It’s very possible that startups in the blockchain space will also be chiseling at the banks’ business, just as dozens of successful FinTech startups have already dissected and unbundled many banking services.

Banks risk being on the outside looking in, if they don’t build on-ramps and exits to the new world of cryptocurrencies. Therefore, they risk becoming islands themselves.

No more warnings from bankers

We don’t need to hear warnings from banking executives about not using bitcoin or cryptocurrencies. In 1995, several banks and financial institutions issued warnings about Internet payments and online commerce as not being safe. Then, a few years later, they all adopted online services and allowed Internet payments. Today, Amazon is bigger than Walmart in market value.

We don’t need to hear that cryptocurrencies are high-risk, because of anonymity, or other factors, just because banking executives don’t fully understand them yet, or because the banks are not yet ready to adopt them.

Business drives technology

We need to remember that “business drives technology choices”, and not the other way around. Business people need to understand technology’s possibilities, and technologists need to better explain what the technology can do.

Only when the two come together with a harmonious understanding will we see real innovations come to life. The opportunities rest on what you make with all existing technologies, based on your willingness to make changes inside your business.

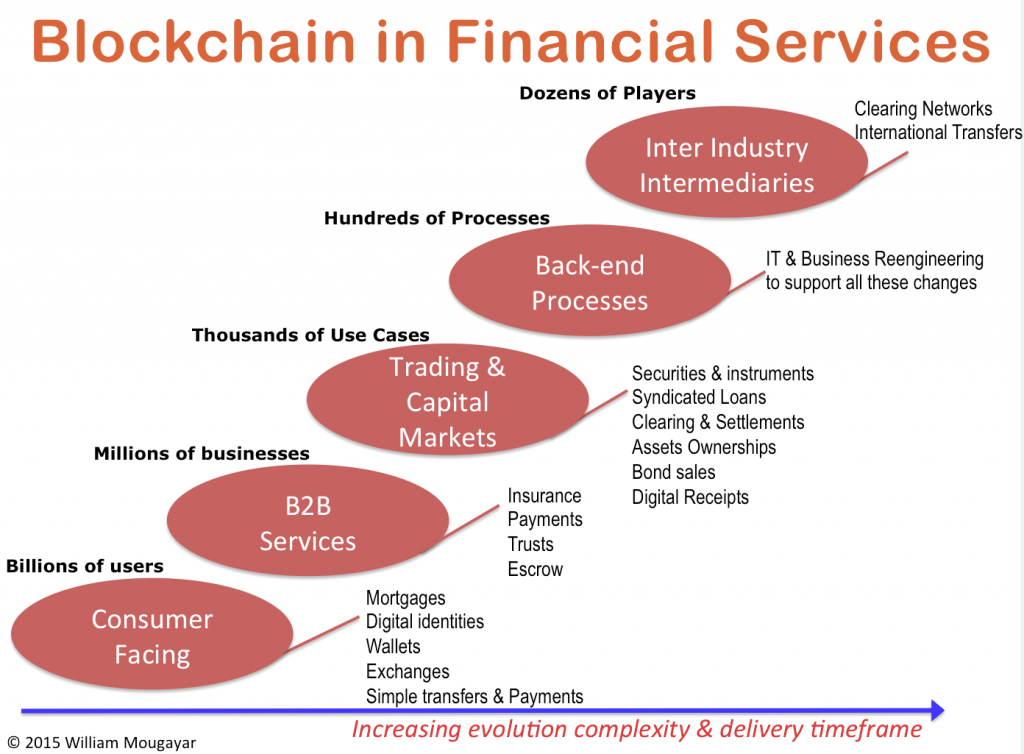

Blockchain Apps are being built to handle the next generation of services in trade settlements, digital ownerships, assets ownerships, assets transfers, origin verification, title transfers, and many other areas.

Here’s a proposed evolution of key application areas, depicting the various touch points and target segments. The broad categories of attention are in consumer services, B2B services, trading and capital markets, back-end processes, and inter-industry services.

There is a lot of work needed to bring this vision to reality. For example, inter-banking co-operation over new networks will not be easy, but it will be done. And reengineering efforts must be taken seriously.

Note that this segmentation is not splitting the market along permissioned (private) vs. permissionless blockchains (public), because that type of demarcation is a technical one.

In reality, there will be a continuum of blockchains, and they will interconnect or interrelate to each other, just as databases do today, in the background, without us knowing about their technical intricacies. So, this is not about blindly ruling out public blockchains in favor of private ones. Rather, you may need to think about using both scenarios, depending on what’s best for each use case.

Putting crypto-tech on the strategic agenda

Where do you start? There are various approaches to get there from an enterprise implementation point of view. Corporate teams need to work with external players and technologies, and many of them are new and in early developmental stages.

Most vendors and technologies have less than a dozen clients at the most, and some have less than a handful. So it is early days for sure, but there is no shortage of innovation. However, the banks must meet these startups half-way by dreaming-up how to apply their technology.

|

Approach |

How it’s done |

Examples |

|

IT Services |

We will build you anything |

IBM & Big IT Firms |

|

Blockchain |

You work directly with the blockchain’s tools and services |

Bitcoin, Ethereum |

|

Development Platforms |

Frameworks for IT professionals |

Eris, Blocknet |

|

Solutions |

Industry-specific |

Clearmatics, Symbiont |

|

APIs & Overlays |

DIY assembling pieces |

Open Assets, Chain |

This field has been maturing at the speed of dog years. And there are new advances pertaining to making it easier to implement decentralization stacks without worrying about building or assembling all of the required pieces from scratch.

Some of the progress being made is equivalent to the evolution from building websites manually using HTML code in 1995 to automagically creating sites today using WordPress and via a few configuration steps.

For example, Ethereum takes care of the complexities of writing decentralization applications so that developers can focus on the desired functionality, and not the intricacies of networked and decentralized peer-to-peer technologies.

Look out for part three in this series, coming soon.

Disclaimer: The views expressed in this article are those of the author and do not necessarily represent the views of, and should not be attributed to, CoinDesk.

Source: www.coindesk.com